Good credit can make a big difference when it comes to things like purchasing a home, getting approved for an apartment, or even how much you’ll pay in interest over time. Credit scores typically range from 300 (minimum) to 850 (maximum) for the widely used FICO and VantageScore models. On average, most Americans have a credit score of around 700, which is considered “good.”

If your credit score isn’t quite as good, tightening up the basics for a few months can often give you a boost. Below are some practical, high-impact steps to focus on. We’ll explain why they work, how to do them, and what kind of improvement you can realistically expect over time.

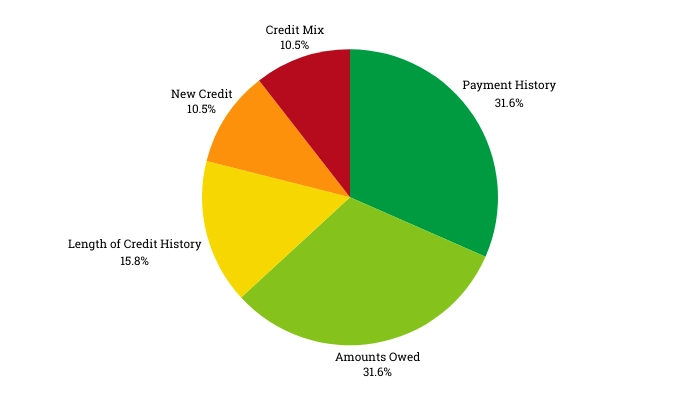

3 factors that will improve your credit score

Pay on time, every time

Late payments are one of the fastest ways to reduce your score, and one of the hardest things to overcome quickly. Payment history accounts for 35% of your credit score.

- Turn on autopay for the minimum on every account (you can still pay extra manually).

- Set a simple reminder a week before due dates.

Consistently paying on time builds trust, and avoiding late payments keeps your score from taking big hits.

Lower your credit card utilization

Utilization is how much of your available card limit you’re using. If you’re carrying high balances compared to your limits, your score can take a hit. The amount you owe accounts for 30% of your credit score.

- Aim for under 30%, and if you can, under 10%.

- Make a payment before the statement closes, not just before the due date. That’s the balance most lenders report.

By doing this, you’re making sure your “reported” balance looks healthier.

Related: How – and why – to check your credit score >>

Pause new applications

Applying for credit creates a hard inquiry, and opening new accounts can temporarily lower your score. New lines of credit account for about 10% of your credit score.

- Don’t apply for new cards/loans for a few months unless you truly need to.

- If you’re in need of a loan, do your homework before submitting applications.

These things reduce risk signals and give your profile time to stabilize. While hard inquiries don’t usually make a huge impact on your credit score on their own, they can add up quickly.

Other factors that affect your credit score

While the three factors above can have the largest impact on your credit score, other variables play into the mix, too. They include:

- Length of Credit History (15%): Considers the age of your oldest account, newest account, and the average age of all accounts; older is generally better.

- Credit Mix (10%): Having a mix of revolving (credit cards) and installment (loans) accounts can be positive.

More tips for boosting your credit score over time

The tips above are great for making a big improvement in your score quickly. However, implementing the following consistently over time can also raise your credit score and ensure it stays where you want it to.

- Check credit reports for errors: Review reports from the three major bureaus (Equifax, Experian, TransUnion) at annualcreditreport.com (1 free report each year) and dispute inaccuracies.

- Don’t close old accounts: The age of your credit matters. Closing old accounts reduces your total available credit, which can increase your utilization ratio.

- Become an authorized user: Getting added to a family member’s credit card with a long, positive history can boost your score.

- Diversify your credit mix: A mix of credit cards and installment loans (like student or auto loans) shows you can manage different types of debt.

- Request a credit limit increase: Asking your card issuer for a higher limit can improve your utilization ratio, provided you do not spend more.

- Use secured credit cards: If you have poor or no credit, a secured card (backed by a deposit) can help build a positive history.

- Report rent and utilities: Services can report your rent, phone, and utility payments to bureaus to build credit.

- Avoid quick-fix scams: Be cautious of companies promising to remove accurate negative information, as only time or legitimate disputes can remove them.

Will doing these things really help my credit score?

Credit scores are basically a risk score. They’re trying to answer one question: How likely are you to pay back borrowed money on time? The score reacts fastest when you improve the inputs that signal “lower risk,” especially:

- You pay on time

- You aren’t maxed out (or close to it) on your credit cards

- You aren’t opening new accounts frequently

When you improve those, your score usually follows. Your credit card balances get reported to the bureaus on a regular schedule, often monthly. So when you lower your balances and keep them low at the moment they’re reported, your score can respond quickly.

Get more help understanding your credit score

And when you’re ready to take the next step, you don’t have to figure it out alone. At Fidelity Federal, our team can help you understand what’s showing up on your credit report, talk through ways to strengthen your profile, and guide you through loan options that fit your goals, whether that’s a vehicle, a home, or a personal loan.

Want more stories like this? Visit our Financial Literacy page for practical resources on credit, budgeting, saving, and smart borrowing.